Flooding on South Claiborne? Your Legal Rights After the Feb 23 Water Main Break

The morning of Monday, February 23, 2026, brought a major disruption to Uptown New Orleans. A 30-inch water main break near the intersection of South Claiborne Avenue and Toledano Street sent water rushing into the streets, flooding businesses and homes, and forcing the closure of over a dozen local schools.

While the Sewerage and Water Board of New Orleans (SWBNO) works to repair the line, many residents are left dealing with property damage, lost business revenue, and the health risks of a wide-ranging boil water advisory.

Two Paths to Recovery: Insurance vs. The SWBNO

When a major main breaks, you are essentially looking at two different "pots" of money for recovery. Understanding the difference is critical to your financial survival.

1. Your Property Insurance: The "Fast" Track

Many homeowners and business owners assume they have to wait for the city to act. However, your own insurance policy may be the fastest way to get money for immediate repairs.

The "Sudden and Accidental" Rule: Most Louisiana policies cover water damage if it is sudden and accidental. A 30-inch pipe rupture is the definition of "sudden."

The "Flood" Distinction: Insurance companies often try to deny these claims by calling them "flooding," which is usually excluded. However, there is a strong legal argument that water from a burst pipe (man-made infrastructure) is a covered peril, unlike rising surface water from a storm.

Timing: Under Louisiana law, your insurance company generally has a duty to initiate your loss adjustment within 30 days of a claim. The SWBNO faces no such deadline.

2. Suing the SWBNO: The "Full" Recovery Track

While insurance might cover the cost of your floors and drywall, it won't cover everything. A legal claim against the city can help you recover:

Your Deductible: The thousands of dollars you had to pay out-of-pocket before insurance kicked in.

Business Interruption: If your shop on Claiborne had to close, insurance may not cover the full extent of your lost profits or "goodwill."

Diminished Value: The long-term loss in property value due to a history of flooding.

Can You Hold the City Accountable?

In New Orleans, recovering damages from a municipal entity like the SWBNO is notoriously complex, but it is possible. Under Louisiana law, specifically the principles established in cases like Saden v. Kirby, the city and its agencies have a clear duty to maintain the infrastructure that protects our neighborhoods.

To win a claim, you generally must prove:

Duty: The SWBNO had a responsibility to maintain the water main.

Breach: They failed to do so (often through negligence or ignoring known issues).

Causation: This failure directly caused the flooding on your property.

Damages: You suffered actual financial or physical loss.

What to Do Immediately if You Were Impacted

If your car was stalled on Claiborne or your property took on water, protect your claim by doing the following:

Document Everything: Take high-resolution photos and videos of the water levels and the damage. Pro Tip: Capture video of the water gushing specifically from the break site toward your property to prove the source.

Keep Your Receipts: Save every receipt for towing, emergency water remediation, or temporary lodging.

File a SWBNO Claim Form: Be aware that the internal SWBNO process often takes 90 days or longer, and many claims are initially denied.

Consult with a Lawyer: Before signing any waivers or accepting a low settlement from an insurance company, speak with a local attorney.

We Are Here to Help

At Montiel Hodge, we know that a "precautionary advisory" or a "temporary closure" is anything but minor when it’s your livelihood on the line. Whether you are dealing with structural damage, ruined inventory, or a denied insurance claim, our team is ready to fight for the compensation you deserve.

Start your claim today!

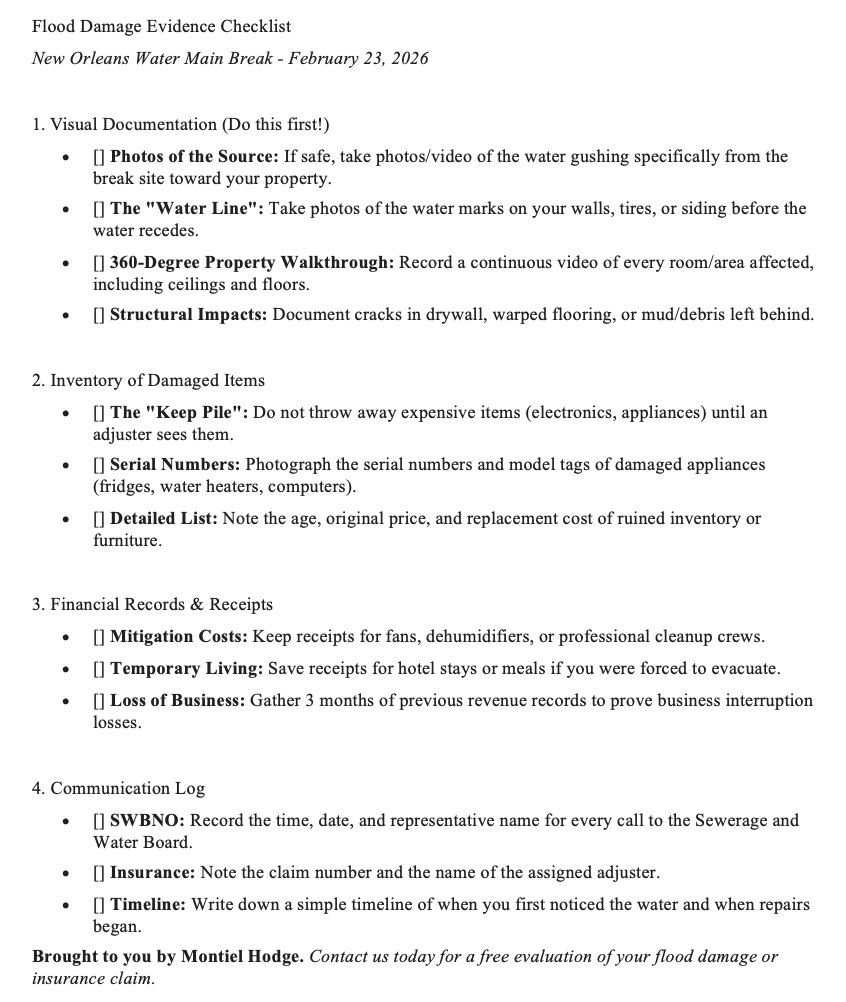

Flood Damage Evidence Checklist